ConsumerLatest.com

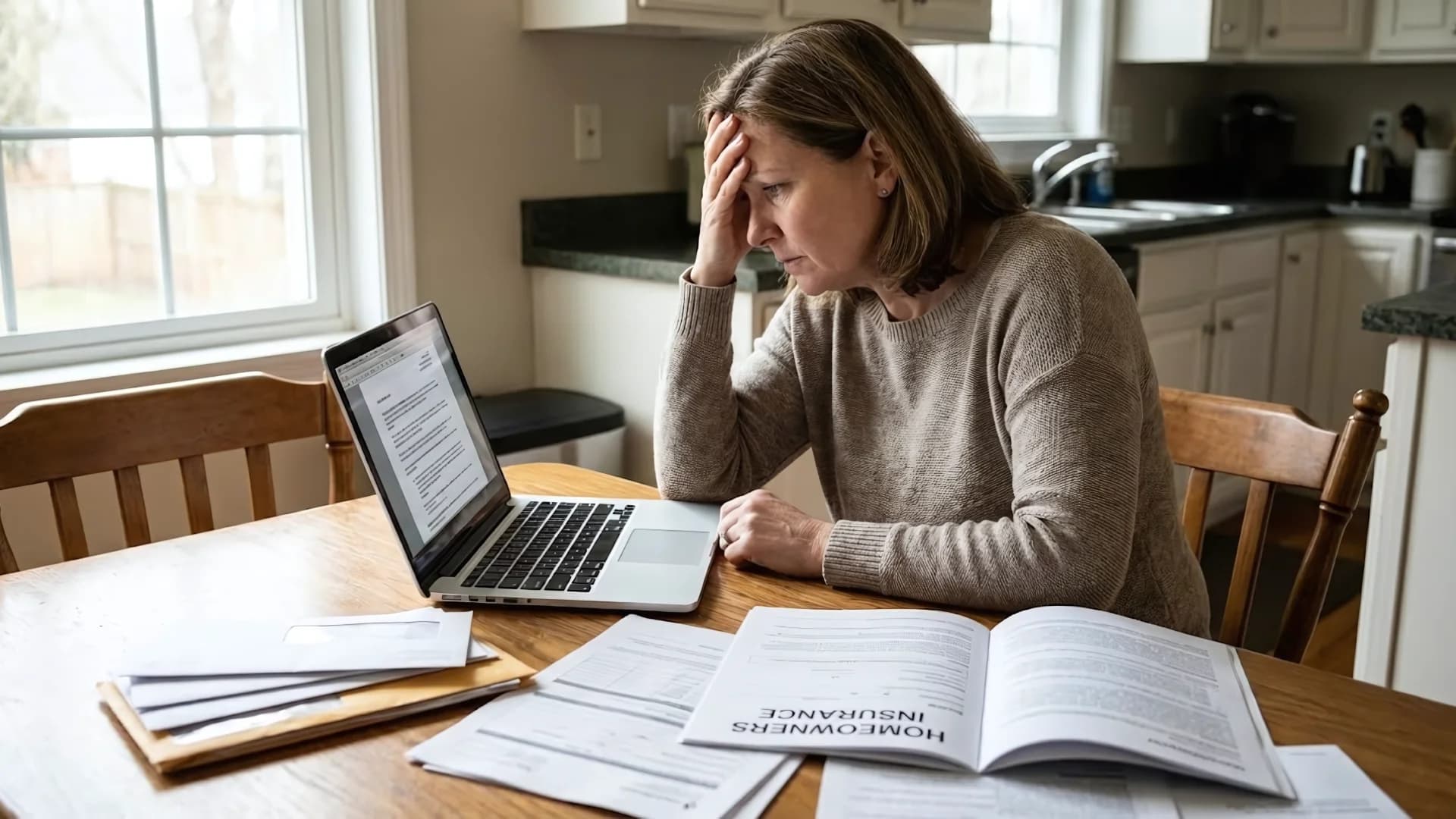

ConsumerLatest.comYour homeowner's insurance renewal arrives. The premium went up again. Maybe 5%, maybe 15%. You grumble, pay it, and move on.

This is exactly what your insurance company is counting on.

Homeowner's insurance is one of those expenses most people set and forget, only paying attention when something goes wrong. That inattention creates a quiet, steady drain on your finances as your insurer gradually raises rates year after year, knowing you probably won't shop around.

Here's how to tell if you're being taken advantage of, and what to do about it.

The Renewal Creep

Look at your insurance premiums over the past five years. If you've been with the same insurer, there's a good chance they've increased 30-50% or more, even if you haven't filed claims or your risk profile hasn't changed.

Insurers raise rates for many reasons: claims experience across their entire book, reinsurance costs, investment returns, and good old-fashioned profit optimization. Your individual circumstances often have little to do with it.

The kicker? New customers are often offered lower rates than loyal customers. You're paying more specifically because the company knows you're unlikely to leave.

The Coverage You Don't Need

Some homeowners are paying for coverage that makes no sense for their situation.

Water backup coverage on a home with no basement and no history of plumbing issues might not be worth the premium. Earthquake coverage in a low-seismic area adds cost without commensurate risk reduction. Excessive personal property coverage beyond what you'd actually replace doesn't help you. Scheduled items (jewelry, art) that you've since sold still inflating your premium is another common issue.

Review your policy line by line. Every coverage item should correspond to a real need in your life.

The Deductible Trap

Many homeowners carry lower deductibles than they should. A $500 deductible might feel safer than a $2,500 deductible, but let's think about this rationally.

With a $500 deductible, you might pay $1,800 per year in premium. With a $2,500 deductible, the premium might be $1,400 per year.

That's $400 per year in savings, or $4,000 over ten years. How many claims do you expect to file in ten years? For most homeowners, the answer is zero or one.

If you have emergency savings that could cover a $2,500 deductible, the higher deductible usually makes financial sense. You're essentially self-insuring small claims and paying less for the privilege.

Shopping Actually Works

I know comparing insurance sounds tedious. But the payoff can be substantial.

When our readers compare rates through services like [HOMEOWNER'S INSURANCE OFFER NAME/LINK], they frequently find that other insurers will offer significantly lower rates for equivalent coverage. Savings of $300-800 annually are common. Some find even more.

The process takes maybe 30 minutes. Enter your information, get quotes from multiple carriers, compare coverage (not just price), and switch if the math makes sense.

That 30 minutes could be worth thousands over the time you own your home.

What to Compare

When shopping, make sure you're comparing like to like. Key elements include dwelling coverage amount (should be the same or similar), personal property coverage limits, liability limits (typically $100,000-300,000), deductible amounts, and additional coverages (water backup, identity theft, etc.).

A policy that's $200 cheaper because it has half the liability coverage isn't actually a better deal. It's a worse policy at a slightly lower price.

When Staying Put Makes Sense

Switching isn't always the right move. You might stay if your insurer has been responsive and fair on past claims (claims handling matters more than premiums), if you have a long relationship with an agent who provides genuine value, if competitor quotes aren't meaningfully better, or if your insurer offers benefits (guaranteed replacement cost, claim forgiveness) that others don't.

But staying should be a conscious choice, not inertia. If you haven't compared rates in more than two years, you're probably overpaying.

The Notification Game

One more thing to watch: cancellation tricks.

Some insurers have been known to "non-renew" policies in high-risk areas or for customers who've had claims. This isn't quite cancellation, but it has the same effect of forcing you to find new coverage, often at worse rates and with less time to shop around.

Read every piece of mail from your insurer. Don't let a non-renewal notice sit unopened until it's too late to respond thoughtfully.

When shopping for new coverage through platforms like [HOMEOWNER'S INSURANCE OFFER NAME/LINK], give yourself plenty of time before your current policy expires.

Final Thoughts

Your insurance company is a business with shareholders to please. They will charge you as much as they can while still keeping your business.

The only way to keep them honest is to periodically remind them that you have options. Shop around, get quotes, negotiate or switch.

They're counting on you not bothering. Don't give them what they want.