ConsumerLatest.com

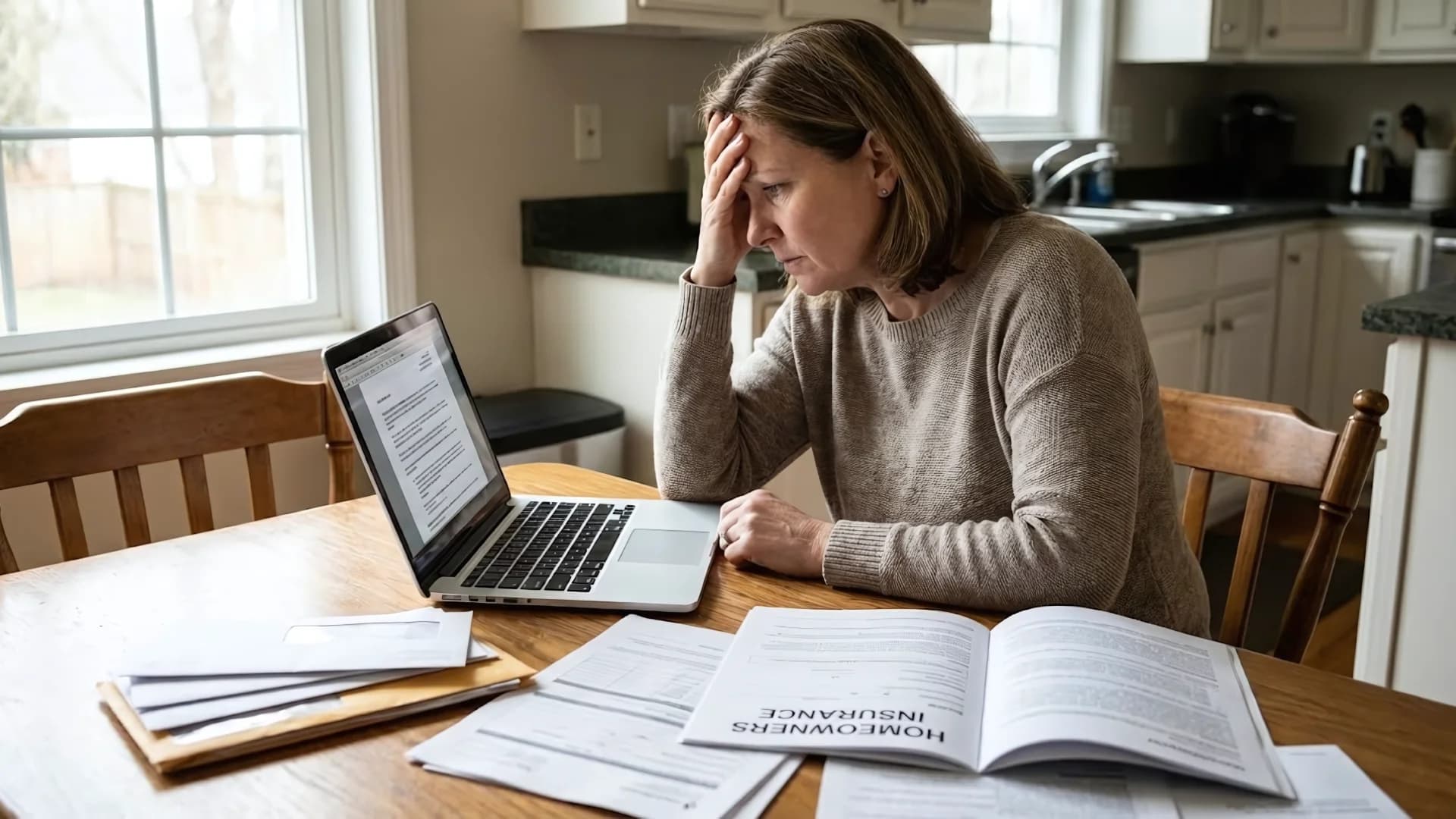

ConsumerLatest.comSomething bad happened to your home. Water damage, fire, storm, theft. You have insurance. Time to file a claim and let the professionals handle it.

Except the claims process is where many homeowners make mistakes that cost them thousands. Your insurance company isn't working against you exactly, but they're definitely not working entirely for you either. They have financial incentives to minimize payouts, and an uninformed homeowner often accepts less than they deserve.

Here's how to avoid the most expensive claims mistakes.

Mistake #1: Not Documenting Thoroughly Before Cleaning Up

Your first instinct after damage is often to start cleaning, to restore normalcy as quickly as possible. But cleaning up before documenting destroys evidence that supports your claim.

Before touching anything, take extensive photos and videos. Document every room, every damaged item, every angle. Include wide shots that show context and close-ups that show detail. If possible, include something for scale reference.

This documentation is your evidence. Insurance adjusters arrive days later and only see what remains. Your contemporaneous documentation shows what actually happened.

Mistake #2: Throwing Away Damaged Items Too Soon

It's tempting to haul damaged items to the curb immediately. Don't.

Your insurer may want to inspect damaged items before agreeing to replacement. Throwing them away can create disputes about what was damaged, how badly, and what it was worth.

Keep damaged items until your claim is settled, or at minimum until your adjuster has inspected and documented them. If you must remove items for safety or sanitation, photograph them thoroughly first.

Mistake #3: Accepting the First Settlement Offer

Insurance adjusters make initial settlement offers. These offers are often lower than what you're entitled to receive. Not always, but often enough that you should never accept immediately.

Review the offer against your policy terms. Does it account for all damaged areas? Does it use replacement cost (if that's your coverage) rather than depreciated value? Does it include all claimed items?

If something seems wrong or missing, push back. Ask for detailed explanations of how the adjuster calculated each component. Request re-inspection if the adjuster missed damage.

You have the right to negotiate. Use it.

Mistake #4: Not Getting Independent Estimates

The insurance company's contractor estimate is not the only relevant number. Get independent estimates from contractors of your choosing.

If your contractor estimates $45,000 to repair damage that the insurance adjuster valued at $32,000, that's a meaningful discrepancy worth discussing. You're not required to use the insurance company's preferred contractors.

Independent estimates give you leverage in negotiations and help ensure you receive enough to actually complete repairs.

Mistake #5: Missing Deadlines

Insurance policies have deadlines for filing claims, documenting losses, and submitting paperwork. Miss these deadlines, and you risk having claims reduced or denied entirely.

Read your policy's requirements. Note all deadlines. Build in buffer time. If you're struggling to meet a deadline, communicate with your insurer before it passes, not after.

Mistake #6: Oversharing or Speculating

When talking to your insurance company, stick to facts you know. Don't speculate about causes, don't guess about values, don't volunteer information that wasn't asked.

This isn't about being dishonest. It's about not unintentionally saying something that can be used to reduce your claim.

If you're not sure about something, say "I don't know" or "I'd have to check." Never make up answers.

Mistake #7: Not Understanding Your Policy

Your policy determines what's covered, what's excluded, what limits apply, and what your responsibilities are. Reading it after a loss is too late but still better than never.

Key things to understand: your dwelling coverage limit, your personal property coverage and any sub-limits for specific categories, your deductible, whether you have replacement cost or actual cash value coverage, and any exclusions that might apply.

If terms confuse you, ask your agent for explanations. Understanding your policy is essential to knowing whether you're being treated fairly.

When to Get Help

For small claims, you can probably navigate the process yourself. For large claims (especially fire, major water damage, or total losses), consider hiring a public adjuster.

Public adjusters work for you, not the insurance company. They understand policy language, documentation requirements, and negotiation tactics. They typically charge 5-15% of your settlement but often increase settlements by more than their fee.

If you're feeling overwhelmed or believe you're being lowballed, a consultation with a public adjuster can be worthwhile.

When dealing with claims and needing to compare new policy options through services like [HOMEOWNER'S INSURANCE OFFER NAME/LINK], understanding your claims history and how it affects your insurability matters.

Final Thoughts

Your insurance company isn't your adversary, but they're not your advocate either. They're a business that benefits from paying less and suffers from paying more.

Being informed, thorough, and persistent is how you ensure your claim is handled fairly. The stakes are too high to be passive.

---

# SAVINGS/PERSONAL FINANCE ARTICLES