ConsumerLatest.com

ConsumerLatest.comTake a close look at your bank and credit card statements from last month. Not just the big transactions. The small ones. The fees.

There's a good chance you're paying for things you didn't know you were paying for, things that don't need to exist, things that better alternatives would eliminate.

These individual fees seem small. $5 here, $12 there. But they add up to hundreds or thousands annually, quietly draining your accounts while you focus on bigger numbers.

The Monthly Maintenance Fee

Many traditional checking and savings accounts charge monthly maintenance fees, typically $5-15 per month.

The stated justification is account upkeep costs. The reality is that plenty of banks offer identical accounts with no monthly fees. You're paying for the privilege of giving a bank your money.

These fees can often be waived by maintaining minimum balances or setting up direct deposit. But even easier: switch to a bank that doesn't charge them at all.

Annual cost of a $12/month maintenance fee: $144. Over ten years: $1,440. For nothing.

ATM Fees (Yours and Theirs)

Use an ATM outside your bank's network, and you typically pay twice: your bank charges you for using an outside ATM, and the ATM operator charges you for using their machine.

These combined fees often run $4-7 per transaction. Use out-of-network ATMs twice a week, and you're paying $400-700 per year just to access your own money.

Some banks reimburse ATM fees (up to certain limits). Others have extensive fee-free networks. Either approach beats paying $5+ every time you need cash.

Overdraft Fees

Overdraft fees are the most expensive fees in banking. A typical overdraft fee is $30-35. If you overdraft by $5 and don't notice for three days, you might pay $35 for what is essentially a $5 short-term loan.

The math on that is obscene: $35 to borrow $5 for three days works out to an annualized interest rate of over 85,000%.

Some banks now offer overdraft protection that links to savings accounts, transferring money to cover shortfalls automatically. Others have eliminated overdraft fees entirely. If you've paid overdraft fees in the past year, it's worth exploring whether better options exist through services like [SAVINGS/PERSONAL FINANCE OFFER NAME/LINK].

Paper Statement Fees

Some banks charge $2-5 per month if you receive paper statements instead of going paperless.

The easy fix: opt for electronic statements. You'll save the fee and have statements that are easier to search and store anyway.

But also worth considering: why bank with an institution that charges you for basic communication?

Minimum Balance Fees

Separate from monthly maintenance fees, some accounts charge additional fees if your balance falls below certain thresholds.

These can be daily fees, weekly fees, or monthly fees, and they stack on top of other charges. A $25 minimum balance fee plus a $12 maintenance fee plus ATM charges can easily hit $50-60 in a single month.

Know your account's requirements. Better yet, choose accounts without these requirements.

Wire Transfer Fees

Need to wire money? Your bank probably charges $25-50 for domestic wires and even more for international transfers.

These fees made more sense when wire transfers required significant manual processing. Today, alternatives like Zelle, Venmo, or other electronic transfers move money instantly or near-instantly for free.

Wire transfers are still occasionally necessary (home closings, certain business transactions), but for most purposes, free alternatives work just as well.

Foreign Transaction Fees

Using your debit or credit card abroad? Many cards charge 2-3% on every foreign transaction.

Spend $3,000 on a European vacation, and foreign transaction fees add $60-90 to your costs.

Many credit cards now offer no foreign transaction fees. Some debit cards from online banks do too. If you travel internationally, switching to a card without these fees is an easy win.

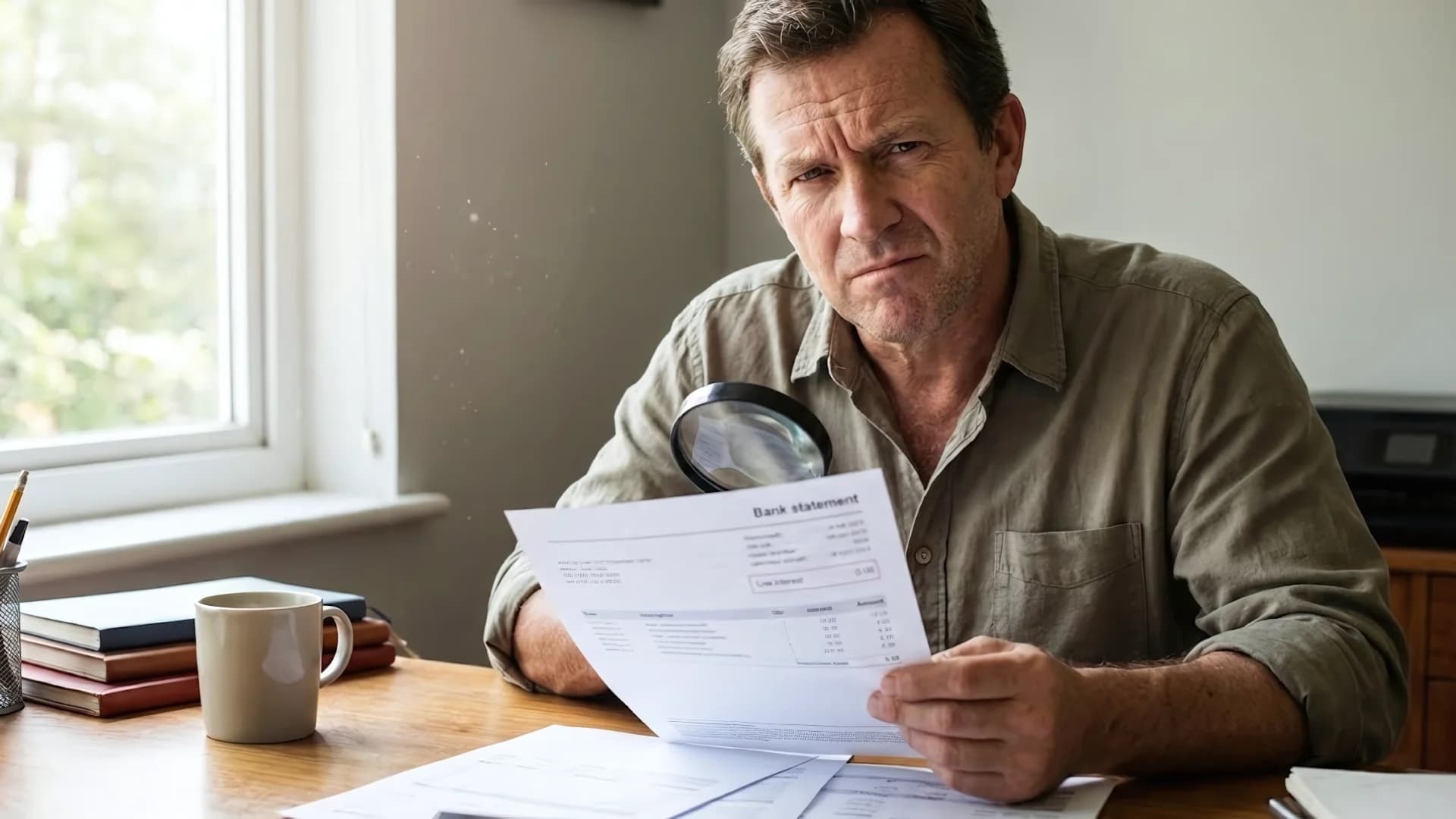

Finding the Hidden Fees

The challenge with bank fees is that they're often not obvious. They're listed in fee schedules that nobody reads, or they show up as small line items easily missed.

To find what you're actually paying, review your statements line by line for three months. Every charge that isn't a purchase you made or a bill you paid is worth investigating.

Once you know what you're paying, you can decide if it's worth switching to fee-free alternatives found through platforms like [SAVINGS/PERSONAL FINANCE OFFER NAME/LINK].

Final Thoughts

Bank fees exist because banks profit from them and customers don't pay attention. The individual amounts seem too small to worry about, so people don't worry about them.

But these small amounts add up. $50 per month in avoidable fees is $600 per year, $6,000 over a decade.

Better alternatives exist for almost every fee you're currently paying. The only question is whether finding them is worth 30 minutes of your time.

It is.