ConsumerLatest.com

ConsumerLatest.comI'm going to share something that most personal finance writers won't tell you: sometimes using your home to pay off debt is the smartest financial move you can make.

I know, I know. The conventional wisdom says never risk your home for unsecured debt. And in many cases, that's good advice. But conventional wisdom doesn't account for the math that trapped me, and possibly you, in a cycle of minimum payments that barely touched the principal.

The Debt Spiral Nobody Talks About

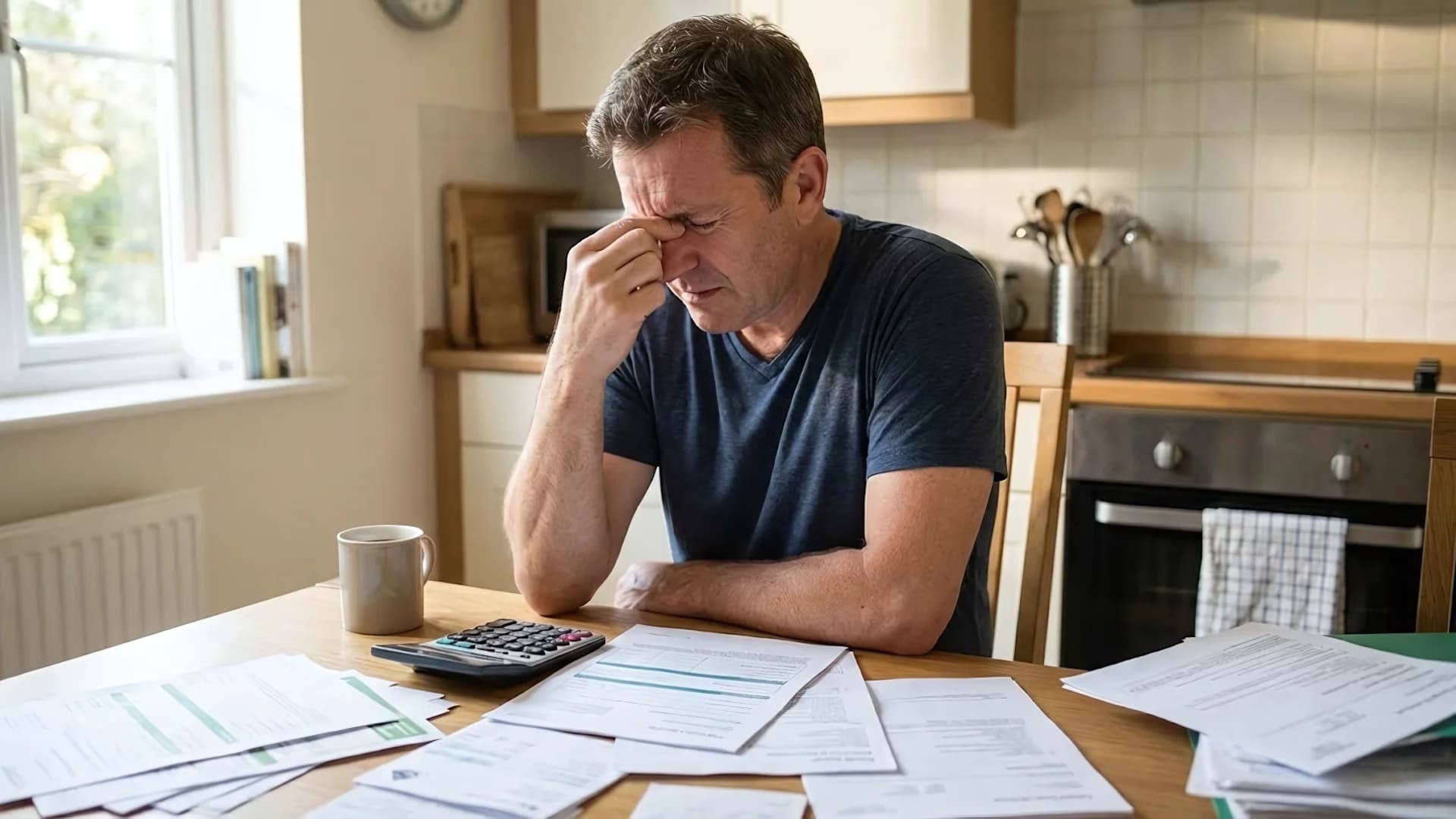

At my worst point, I had $47,000 spread across six credit cards. Average interest rate: 22.4%. My minimum payments totaled about $1,175 per month, and roughly $875 of that went straight to interest. Every single month.

I did the calculation one sleepless night: at minimum payments, I'd be debt-free in 27 years and would have paid over $83,000 in interest alone.

I wasn't buying luxury goods. Medical bills from my daughter's emergency surgery. A job loss that lasted four months. Car repairs that couldn't wait. Life happened, and the credit cards were there, and suddenly I was drowning.

The HELOC Solution

Here's what changed everything. My home, which I'd owned for eight years, had appreciated significantly. I owed $195,000 on a house now worth $340,000. That meant I had roughly $145,000 in equity, and I'd never really thought about what that meant in practical terms.

After researching my options through services like [HELOC OFFER NAME/LINK], I discovered I could access up to $77,000 through a home equity line of credit at an interest rate around 8.5%.

Let's compare:

Credit card debt: $47,000 at 22.4% average = approximately $875/month in interest HELOC: $47,000 at 8.5% = approximately $333/month in interest

That's $542 per month that could go toward actually paying down the principal instead of disappearing into interest payments.

The Numbers After One Year

I took the full $47,000 from my HELOC and paid off all six credit cards the same day. I kept one card open for emergencies but cut up the rest.

My new HELOC payment: $398/month (interest plus a small amount toward principal)

I committed to paying $800/month instead, roughly what I was paying in minimums before, but with a crucial difference: now most of that payment actually reduced my debt.

After 12 months:

- Total paid: $9,600

- Interest paid: approximately $3,700

- Principal reduced: approximately $5,900

- Remaining balance: $41,100

Compare that to the credit cards, where the same $9,600 in payments would have reduced my principal by maybe $3,600 while the rest vanished into interest.

The Psychological Shift

Something else happened that I didn't expect: the HELOC forced me to confront my spending in ways the credit cards never did.

When you have six cards, it's easy to lose track. A charge here, a balance transfer there, promotional rates expiring without you noticing. The HELOC is one number. One payment. One balance that either goes up or down based on my choices.

I check it weekly now. I've become obsessive about watching that number shrink.

The Risk I Accepted

I'm not going to pretend there's no risk here. My home now secures this debt. If I default, I could eventually lose my house. That's serious, and I thought long and hard before making this decision.

But here's my honest calculation: I was never going to default on mortgage payments while simultaneously making $1,175 in credit card minimums. If financial catastrophe struck, the credit cards would have been the first thing I stopped paying. Now, my total housing-related debt (mortgage plus HELOC) carries a payment I can manage even in a worst-case scenario.

Is This Right for You?

This approach makes sense if you have significant home equity, you're disciplined enough to avoid new credit card debt, your income is stable enough to handle the HELOC payment, and the interest rate difference is substantial (it usually is).

It doesn't make sense if you're still in a spending pattern that created the debt, you're planning to sell your home soon, or you'd only be marginally lowering your rate.

When I compared options through platforms like [HELOC OFFER NAME/LINK], I made sure to factor in all the fees and closing costs to ensure the math actually worked in my favor.

Final Thoughts

Two years from now, I'll be debt-free. Not 27 years. Two years. The HELOC transformed an impossible situation into a concrete payoff date I can actually see on my calendar.

I'm not saying this is right for everyone. But for those trapped in high-interest debt with equity sitting unused in their homes, it's worth running the numbers. Sometimes the unconventional path is the smartest one.